Most DTC brands hit a wall between $20M and $50M, and it is a channel problem, not a demand problem. Pure-play DTC runs out of road before $100M because paid acquisition gets more expensive with every dollar, with CAC up roughly 60% over five years. The way through is omnichannel: wholesale, retail, and marketplaces alongside DTC, not instead of it.

- Brands combining online, retail, and wholesale see blended acquisition around $25 to $50, against $45 to $150 for DTC-only.

- Omnichannel retention averages around 89%.

- The fix is not a better Meta strategy; it is more channels working together.

There's a wall most direct-to-consumer brands hit somewhere between $20M and $50M, and it isn't a demand problem. It's a channel problem. Pure-play DTC, the online-only model that built a thousand brands in the 2010s, runs out of road well before $100M, because the single engine that got you there, paid acquisition, gets more expensive with every dollar you add. Customer acquisition costs have climbed roughly 60% over the last five years, and at the top of the funnel the audiences are saturated. The curve flattens, the math stops working, and the brand stalls.

The way through isn't a better Meta strategy. It's omnichannel: wholesale, retail, and marketplaces operating alongside DTC, not instead of it. The data is hard to argue with. Brands that combine online, retail, and wholesale tend to see blended acquisition land in the $25 to $50 range, against $45 to $150 for DTC-only. Retention with omnichannel engagement averages around 89%, versus 33% for single-channel. And in M&A, hybrid models routinely earn the highest multiples in the category. The brands that scaled to $100M and beyond, On, HOKA, Warby Parker, Vuori, almost all of them stopped being pure-play a long time ago.

I lived this transition at WIN Brands Group. We built brands online and then pushed them into wholesale and retail, and I ran the blended-CAC models, negotiated the first accounts, and absorbed the margin hit that comes with selling through someone else's shelf. The hardest part wasn't deciding to go omnichannel. It was the sequence and the tradeoffs: which channel to add, when, and what it does to your margin and your control. Get that wrong and omnichannel becomes a drag on the business instead of the thing that unlocks the next phase.

This is the long version of that playbook. Why pure-play hits a ceiling, why the "death of DTC" headlines are half right, how omnichannel actually lowers blended CAC and lifts retention, the real margin and control tradeoffs of each channel, the sequence from DTC to wholesale to retail to marketplaces, what the brands that pulled it off can teach you, and why hybrid models command the best exit multiples. If your brand is parked on the DTC plateau, this is the map off it.

The ceiling pure-play

DTC hits, and why

it isn't demand.

The pure-play ceiling shows up most often between $20M and $50M, and it's a function of the acquisition model, not the market. A DTC brand built entirely on paid social and search has one real growth lever: spend more to acquire more. That works beautifully while the audiences are fresh and the ad costs are low. It stops working when the obvious channels saturate and each incremental customer costs more than the last one did, until the marginal customer costs more than they're worth.

This is the trap that caught a whole generation of brands. Digital ad spend at struggling DTC darlings often consumed 30% to 40% of revenue, a number that's survivable at small scale and fatal at large scale, because there's no operating model underneath it that improves as you grow. The brand isn't running out of customers. It's running out of affordable customers, which is a very different and much more dangerous problem, because it looks like a marketing issue right up until it becomes an existential one.

The structural reason is signal loss and platform concentration. When most of your acquisition runs through two ad platforms, you're a price-taker in an auction that gets more crowded every year. Privacy changes degraded targeting, more brands bid for the same eyeballs, and CPMs climbed. None of that is cyclical. It's the steady-state cost of building a business on rented audiences you don't own and can't control, which is exactly why the brands most exposed to it stalled first.

Here's the part founders underrate. The ceiling isn't a hard stop, it's a slow grind, and that's what makes it so dangerous. Revenue keeps inching up, so it doesn't feel like a wall. But the unit economics quietly deteriorate underneath the growth, because you're buying that growth at a worse and worse price. By the time the P&L makes the problem obvious, you've often spent two years and a lot of capital pushing on a lever that was never going to get you to $100M. The brands that scaled past it didn't push harder on paid. They added engines.

I watched this from the operator's seat. A brand can look healthy at $25M and be quietly trapped, growing 15% a year on acquisition costs that rise faster than revenue, with a founder convinced the fix is a better creative strategy or a new agency. It almost never is. The fix is structural: you have to add sources of customers that don't carry a click cost, which is the entire argument for omnichannel and the reason the smart money stopped treating DTC as a complete business model somewhere around the predictable inflection points where DTC brands stall.

There's a second, sneakier version of the ceiling worth naming, because it traps the brands that are good at marketing. A skilled team can keep paid acquisition working longer than it should by getting better at creative, broadening audiences, and squeezing the funnel. That's genuine skill, and it buys time. But it also masks the structural problem, because the brand keeps growing on paid right up until it suddenly can't, and then the fall is steeper because there was no second engine being built in the background. The most dangerous place to be isn't a brand that's obviously stalled. It's a brand that's still growing on paid alone and has therefore never felt the urgency to diversify. By the time the urgency arrives, building wholesale or retail from scratch takes 12 to 24 months you no longer have.

The honest framing is that pure-play DTC was never a finished business model. It was a brilliant launch model, the fastest, cheapest way in history to start a brand, reach customers directly, and learn what sells without a buyer or a distributor as gatekeeper. That's still true and still valuable. The error was mistaking the launch model for the scale model, and assuming the thing that got you to $10M would keep working to $100M. It won't, not because DTC is bad, but because no single acquisition channel survives being asked to carry an entire nine-figure business by itself.

"Pure-play DTC doesn't run out of customers. It runs out of affordable ones, and that's a structural problem no creative strategy fixes."

Is DTC dead? Half

the headline is

true.

The "death of DTC" headline is half right, and the half it gets wrong is the half that matters. Pure-play DTC as a standalone path to scale is genuinely struggling. But DTC as a channel, a launchpad, and a way to own the customer relationship is healthier than ever. The proof is in the behavior of the brands themselves: 82% of DTC brands above $50M now run a physical retail presence. They didn't abandon direct. They stopped being only direct.

The brands that got declared dead, Casper, Allbirds, Peloton, weren't killed by direct-to-consumer. They were killed by trying to scale it profitably on paid traffic alone, and by treating physical retail as an afterthought instead of a core channel. Allbirds ended up shuttering stores and pivoting markets to a distributor model. Casper's stock fell more than 50% from its IPO price. Their failures were channel-architecture failures, not proof that selling directly to customers is a bad idea.

Look at the counterexample sitting right next to them. Warby Parker expanded profitability in 2025 and posted its seventh straight quarter of accelerating active-customer growth, and it did it on the back of roughly 900 retail locations layered on top of its original online model. Same category pressures, same rising ad costs, completely different outcome, because Warby treated retail as a primary channel from early and built an omnichannel machine instead of an online-only one.

So what actually died? The thesis that you could build a durable nine-figure consumer business on rented digital audiences with no owned distribution. That thesis is dead, and good riddance, because it was always a financing trick dressed up as a business model. What replaced it is the realization that DTC is one channel in a portfolio. It's the best place to launch, the best place to learn, and the best place to own the relationship. It is not, on its own, the whole company.

The reframe matters because it changes what you do next. If you believe DTC is dead, you panic and chase the next shiny acquisition channel. If you understand that pure-play is what's dead, you do something calmer and more durable: you keep DTC as your core and your launchpad, and you build the other channels around it deliberately. That's not a retreat from direct. It's a graduation from depending on it for everything.

The acquisition math

that quietly breaks

the model.

The math that breaks pure-play DTC is the relationship between what a customer costs to acquire and what they're worth, and it breaks because one side keeps rising while the other stays flat. When DTC-only CAC runs $45 to $150 and keeps climbing, but your average order value and repeat rate hold steady, the gap between acquisition cost and customer value narrows every quarter until it closes. That's the whole crisis, compressed into one sentence.

The discipline that should govern this is a ceiling, not a target. Every brand has a maximum allowable CAC, the most you can pay to acquire a customer and still make the unit economics work, and pure-play brands routinely blow past it in pursuit of growth. The trouble is that the ceiling is set by your margin and your retention, both of which a single-channel brand struggles to improve, so the ceiling doesn't move up to meet the rising cost. It just sits there while the cost sails over it.

This is where omnichannel changes the equation, and it's worth being precise about how. Omnichannel doesn't lower the CAC of your Meta campaigns; those stay expensive. What it does is add customers acquired through channels with a much lower or even zero click cost, which pulls your blended CAC down. A wholesale buyer didn't cost you a paid click. A customer who discovers you in a store and then buys online later attributes to "direct" in your analytics. Mix enough of those cheaper customers in, and the blended number drops into the $25 to $50 range even though your paid CAC never moved.

That blended math is the difference between a model that compresses and one that breathes. A brand acquiring everyone through paid is at the mercy of the auction. A brand acquiring a third of its customers through wholesale, a chunk through retail foot traffic, some through marketplace discovery, and the rest through paid has a blended cost that's structurally lower and far less exposed to any single platform's pricing. You've turned one fragile input into a diversified portfolio, and diversified inputs are always cheaper and steadier than concentrated ones.

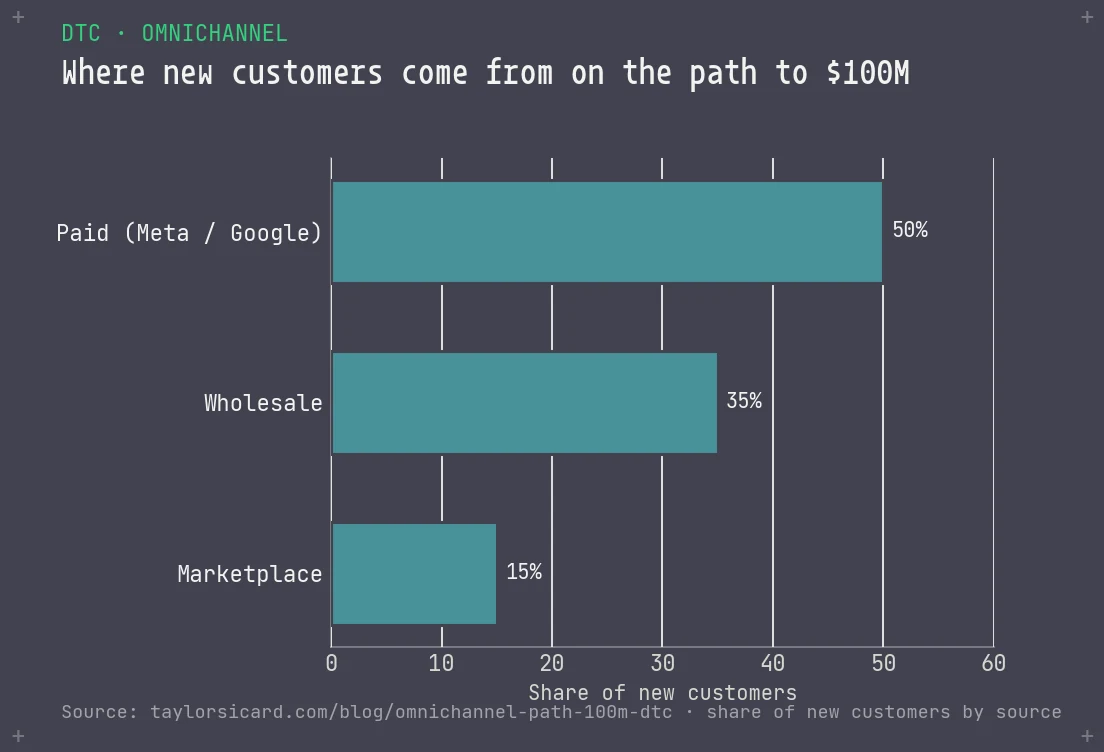

It's worth walking through a concrete version so the mechanism is vivid. Imagine a brand at $30M acquiring entirely through paid, with a $120 CAC and the cost rising 10% a year. Their growth is real but their unit economics are quietly eroding, and every board meeting is a debate about creative. Now imagine they add wholesale and one marketplace, so that within 18 months 35% of new customers come through wholesale at effectively no acquisition cost, 15% through marketplace at a fee rather than a click, and only 50% still through paid. Even if the paid CAC keeps climbing to $135, the blended number lands well below the old all-paid figure, then keeps falling as the cheaper channels grow. Same brand, same product, completely different trajectory, and the only thing that changed was the channel mix feeding the top of the funnel.

| Customer source | Share of new customers | Effective acquisition cost | Weighted contribution to blended CAC |

|---|---|---|---|

Paid (Meta / Google) Rising auction cost | 50% | ~$135 | ~$68 |

Wholesale No per-customer click cost | 35% | ~$0 | ~$0 |

Marketplace Fee per sale, high intent | 15% | ~$25 | ~$4 |

Blended result What actually predicts scalability | 100% | · | ~$72 and falling |

The deeper point is that paid CAC is the wrong number to obsess over once you're scaling. Founders fixate on it because it's the number their ad platform shows them every day, but it's a single-channel metric in a multi-channel world. The number that actually predicts whether you can keep growing profitably is blended CAC against blended contribution margin, read together. A brand that manages to the channel-level paid number is optimizing one instrument on a dashboard while the plane's overall fuel efficiency goes unwatched. The whole shift to omnichannel is, in part, a shift to managing the blended numbers instead of the channel-level ones.

A warning before you celebrate a falling blended CAC: the number can drop for the wrong reasons. If wholesale starts to dominate the mix, your blended CAC looks fantastic while your gross margin quietly collapses, because wholesale carries a far lower margin per unit. A healthy blended CAC has to be read alongside blended contribution margin, never on its own. The brands that get this wrong chase the cheapest customer instead of the most profitable one, and end up with a great-looking acquisition number on a worse business. Track both, and judge channels on contribution after CAC, not on CAC alone.

How adding channels

actually pulls the

cost down.

Omnichannel lowers blended CAC through three distinct mechanics, and it helps to separate them, because they work on different timelines. First, channel substitution: wholesale and marketplace customers arrive with little or no per-customer acquisition cost on your side, so adding them mechanically dilutes the expensive paid customers in your blend. Second, the halo effect: physical presence makes every other channel convert better. Third, owned discovery: a store or a wholesale shelf is a billboard you don't pay a CPM for.

The halo effect is the one founders consistently underestimate. When a brand opens a store in a market, its online sales in that market reliably rise, because the store builds awareness and trust that the website then converts. The store isn't just selling to walk-ins; it's lowering the cost of every online customer in its trade area by warming them up first. That's why Warby and Vuori talk about retail as brand-building, not just as a sales channel. A store full of customers is the cheapest advertising you'll ever run, and it shows up as a lower paid CAC everywhere around it.

Wholesale does something similar through a different door. When your product sits on the shelf at a respected retailer, two things happen: you reach customers who would never have clicked your ad, and you borrow the retailer's credibility. The customer who discovers you at a specialty store and then becomes a loyal direct buyer cost you a wholesale margin, not a paid click, which is usually the better trade. This is the hidden revenue channel a lot of DTC founders ignore because it feels like a step backward, when it's often the cheapest growth available to them.

Marketplaces add a third source of cheap discovery, with their own tradeoffs. A customer searching for your product category on a major marketplace is high-intent and ready to buy, and capturing them there costs you a marketplace fee rather than a top-of-funnel ad spend. The catch is that you don't own that customer or their data, so marketplaces are best used as a discovery and incremental-volume channel rather than a core, and tools like supply-side collectives are starting to give brands marketplace-style reach without fully surrendering the relationship.

Put the three together and the blended math becomes obvious. You're not making paid acquisition cheaper. You're making paid acquisition a smaller slice of a larger, more diversified pie, and the rest of that pie is filled with customers who cost you margin or fees instead of clicks. That's how a brand with a $120 paid CAC ends up with a $40 blended CAC, and why the blended number is the one that actually predicts whether you can scale.

Why omnichannel

customers come

back more.

Lower CAC gets the attention, but the retention story is the one that actually compounds, and the numbers are striking. Customer retention with omnichannel engagement averages around 89%, while single-channel retailers retain roughly 33%. That's about 2.7 times the retention, and retention is the lever that quietly decides whether your acquisition spend ever pays off, because a customer who comes back carries almost no acquisition cost the second, third, and fourth time.

It's not just that they stay; they spend more and shop more often. Omnichannel shoppers deliver roughly 30% higher lifetime value than single-channel shoppers, spend about 16% more per order, and shop around 70% more frequently. Even converting one existing single-channel customer to omnichannel tends to lift their basket size and frequency. The customer who buys from you online and in store, who follows the brand across surfaces, is simply a more valuable customer, and omnichannel is how you create more of them.

Why does shopping across channels make a customer stickier? Because every additional touchpoint is another thread tying them to the brand. A customer who only ever sees you in a Meta feed has one fragile connection that a single algorithm change can sever. A customer who bought in your store, reorders on your site, and runs into you on a retailer's shelf has multiple reinforcing reasons to stay loyal. You've moved from a transactional relationship to a habitual one, and habit is the foundation of the LTV math most brands get wrong.

This compounds directly into the CAC problem from the last section. A brand with 89% retention can afford to pay more to acquire a customer than a brand with 33% retention, because each customer is worth so much more over their life. So omnichannel attacks the acquisition math from both ends at once: it lowers the blended cost of acquiring a customer, and it raises the value of the customer you acquire. Those two forces multiply rather than add, which is the real reason omnichannel brands can keep scaling past the point where pure-play brands stall.

There's a retention nuance worth flagging, though. Omnichannel retention is high partly because omnichannel customers self-select; the most engaged customers are the ones who shop you everywhere. You can't simply bolt on a channel and expect 89% retention overnight. The number reflects a brand that has earned multi-channel loyalty, not a brand that just opened a second sales surface. The work is in giving customers genuine reasons to engage across channels, and pairing that with the retention mechanics that keep them coming back, not in the channel count alone.

The practical implication is that the retention gain has to be designed for, not assumed. The brands that capture it build genuine connective tissue between channels: a loyalty program that recognizes the same customer in a store and on the site, post-purchase flows that bring an in-store buyer back to the website, a product experience consistent enough that a customer who discovers you on a shelf knows exactly what to expect when they buy direct. That's the work behind the 89%. A brand that opens a store and a wholesale account but treats each as a separate silo, with no shared identity or data, captures the reach but leaves most of the retention compounding on the table. Omnichannel done as a set of disconnected channels is just multi-channel; the retention payoff comes from making the channels feel like one brand to the customer moving between them.

The channel map: CAC,

margin, control, and

the role each plays.

Not all channels are interchangeable, and the mistake brands make is treating "omnichannel" as a single thing rather than a portfolio with distinct roles. Each channel trades off acquisition cost, margin, and control differently, and each one earns its place in the mix for a specific reason. Here's how the four core channels actually compare, and what job each one is best suited to do.

| Channel | Customer cost | Margin | Control | Role in the mix |

|---|---|---|---|---|

DTC (owned) Site, paid + organic | $45–$150 paid CAC | Highest (≈57% median GM) | Total | Launch, learn, own the customer, set the brand |

Wholesale Sell through retailers | Low / no click cost | Lowest (≈40–50% off list) | Low | Reach, awareness, scale volume, lower blended CAC |

Owned retail Your stores, pop-ups | High fixed cost, halo upside | High, but heavy overhead | Total | Brand-building, experience, halo on every channel |

Marketplaces Amazon and similar | Fee per sale (≈25–40%) | Squeezed by fees | Lowest (no data) | High-intent discovery, incremental volume |

DTC is the anchor, and nothing else changes that. It carries the highest margin, gives you total control of the experience and the data, and it's where you launch products, learn what works, and own the customer relationship outright. The cost is acquisition: it's the channel most exposed to rising CAC, which is exactly why it can't be the whole company. Think of DTC as your headquarters, not your only building.

Wholesale is the volume and reach play, and it trades margin for scale. Selling through a retailer typically means giving up 40% to 50% off your list price, so the per-unit margin is the lowest in the mix. But the customer cost is near zero, the reach is enormous, and the awareness it builds lowers your CAC everywhere else. Wholesale is how you put product in front of customers who would never click an ad, and how you borrow a retailer's credibility while building your own.

Owned retail is the brand-building and halo channel, and it's the most expensive to run and the most powerful when it works. Stores carry real fixed costs, rent, staff, build-out, so they demand volume to pay off. But they deliver the experience that builds loyalty, and the halo effect that lifts every other channel in their trade area. Marketplaces round out the portfolio as a high-intent discovery channel: a place to capture ready-to-buy demand for incremental volume, at the cost of fees and, importantly, the customer data you'd otherwise own. Each channel does a job the others can't, which is the entire point of running them together rather than betting on one.

The framing that helps most is to stop asking which channel is "best" and start asking what job you're hiring each one to do. DTC is hired to launch and to own the relationship. Wholesale is hired to lower blended CAC and put product in front of customers paid can't reach. Retail is hired to build the brand and create the halo. Marketplaces are hired to catch high-intent demand you'd otherwise miss. Once you see them as a roster of specialists rather than competing options, the apparent contradictions resolve: of course wholesale has a worse margin than DTC, that's not its job; its job is reach and blended-cost dilution, and it does that better than any other channel you have.

The mistake I see most often is brands trying to make every channel do the same job, usually maximize margin, and then concluding that the lower-margin channels aren't worth it. That's like benching your best defender because he doesn't score. Wholesale isn't there to deliver DTC margins; if it did, it wouldn't deliver DTC-scale reach. Retail isn't there to be cheap; it's there to do the brand work no ad can do. When you evaluate each channel against the job it's actually there to do, rather than against DTC's margin profile, the portfolio logic becomes obvious and the resistance to "diluting" your margin fades.

There's also a portfolio-balance question that's easy to miss. The healthiest omnichannel brands rarely let any single channel dominate to the point of dependence, even a high-margin one. A brand that's 90% DTC is fragile to acquisition costs; a brand that's 90% wholesale is fragile to a single retailer's buying decisions and has given away its customer relationship; a brand that's 90% marketplace has handed its fate to a platform. The target isn't to maximize any one channel. It's a deliberate spread, weighted toward the channels that fit your category, that no single shock can topple. Balance is the goal, not optimization of any single line.

What you give up

for the volume

each channel adds.

Omnichannel isn't free, and pretending otherwise is how brands stumble into it badly. Every channel beyond DTC trades something away, usually margin or control, for what it adds in reach or volume. The counterintuitive part, and the one that catches founders, is that the channel with the lowest per-unit margin can still be the most profitable addition once you account for what it does to your blended CAC and your overhead. You have to do the full math, not the per-unit one.

Start with the raw margin picture, because it's stark. DTC runs a median gross margin around 57% for public consumer brands. Sell the same product through a marketplace and you're often looking at 30% to 50% gross after combined platform and fulfillment fees of 25% to 40%. Wholesale lands lower still on a per-unit basis, since you're typically selling at 40% to 50% off list. On paper, every channel you add dilutes your gross margin, which is why a margin-obsessed founder resists them.

But here's the twist that reframes the whole decision. Industry analysis has actually found DTC operating margins running meaningfully below wholesale operating margins, because DTC carries the full weight of acquisition, fulfillment, returns, and customer service that a wholesale unit shifts onto the retailer. The high gross margin of DTC is partly an illusion that disappears once you load all the costs the channel actually bears. Wholesale gives up gross margin but sheds a pile of operating cost, and the operating margin can end up comparable or better. This is why contribution margin, not gross margin, is the right lens for evaluating any channel.

The control tradeoff is the other half, and it's subtler than the margin one. Wholesale and marketplaces hand you reach but take your relationship with the customer. You don't get the data, you don't own the experience, and in the case of marketplaces you're exposed to a platform that can change its rules, its fees, or its own competing products at will. A brand that becomes 70% dependent on a single marketplace has traded control for volume in a way that quietly caps its value, which is the same concentration risk that shows up across any serious channel-mix strategy.

So the discipline is to add channels for their job, not their headline margin. Wholesale earns its place by lowering blended CAC and building awareness, even though its per-unit margin is thin. Marketplaces earn their place by capturing high-intent demand you couldn't reach otherwise, even though the fees bite. Retail earns its place through the halo and the loyalty, even though the overhead is heavy. Judge each channel on its full contribution to the blended business, after CAC, after operating cost, after the halo it creates elsewhere. Done that way, the "low-margin" channels are frequently the ones that make the whole portfolio more profitable.

One tradeoff deserves a closer look, because it sinks more omnichannel pushes than any margin number: operational complexity. Running four channels well is genuinely harder than running one. Wholesale demands EDI, line sheets, terms, and a sales motion most DTC teams have never built. Retail demands real estate, staffing, and inventory in physical locations. Marketplaces demand their own catalog discipline and fee management. Each channel adds operational surface area, and a brand that bolts them on without the systems and people to run them ends up with four mediocre channels instead of one strong one. The margin math can be perfect and the execution can still fail, which is why sequencing and capability-building matter as much as the strategy.

This is also where inventory gets dangerous. A single-channel brand has one demand signal to forecast against; an omnichannel brand has to allocate the same inventory across DTC, wholesale orders, retail floors, and marketplace demand, each with different lead times and different penalties for getting it wrong. Wholesale especially can whipsaw you, a big purchase order looks like a windfall until the retailer marks it down, returns it, or doesn't reorder, and you're sitting on inventory you built for a channel that didn't repeat. The brands that scale omnichannel cleanly invest in the demand-planning and inventory discipline to feed every channel without starving or drowning any of them. The strategy is the easy part; the operational maturity to execute it is the moat.

"The channel with the lowest per-unit margin can be the most profitable thing you add, once you count what it does to your blended cost."

The sequence: DTC to

validate, then build

the rest.

The single most important thing about omnichannel is the order you do it in, because adding channels in the wrong sequence is how brands lose money on the way to scale. The pattern that works, and the one I've run, is to use DTC to validate, then layer the other channels deliberately as the brand earns the right to each one. The omnichannel inflection usually lands between $20M and $50M, and almost every $30M-plus brand is planning, building, or rebuilding its first major wholesale or retail push within 24 months.

Why first: DTC is the only channel that gives you the unfiltered customer feedback and first-party data to know what's actually working. You earn the right to wholesale and retail by proving demand here first, because no retailer wants to be your test market.

Why here: This is the inflection band where paid starts to choke. Marketplaces and wholesale add cheaper customers exactly when DTC acquisition is getting expensive, and a strong first wholesale account is proof of demand you can build the next phase on.

The payoff: A brand running DTC, wholesale, retail, and marketplaces in concert has diversified revenue, a structurally lower blended CAC, retention that compounds, and the channel architecture that earns the highest exit multiples in the category.

A few notes on doing this well. Don't skip the validation phase to chase wholesale early; a retailer that takes your unproven product and watches it sit on the shelf does more damage than the revenue was worth. Start wholesale narrow and right, the specialty retailers whose customers are your customers, before going wide. And treat pop-ups and shop-in-shops as the low-risk way to test owned retail before you sign a long lease, because they let you learn the halo math without the fixed-cost commitment. The sequence works because each phase de-risks the next, which is the same logic behind the inflection-point discipline that separates brands that scale from brands that stall.

One more thing the sequence protects you from: building omnichannel for vanity. Adding channels because competitors have them, rather than because the math calls for them, is how brands end up with a complicated business that's less profitable than the simple one they had. Each channel should be added when the brand has earned it and the numbers support it, not because an omnichannel deck looks impressive. The discipline is in the timing, not just the ambition.

What Warby, Vuori,

On, and HOKA

actually did.

The brands that scaled past the pure-play ceiling all did the same fundamental thing, layering channels onto a strong DTC core, but each one teaches a slightly different lesson worth stealing. Looked at analytically rather than as logos to admire, they're a field guide to the sequence in this post, and to the specific tradeoffs each channel forces. Here's what each one actually got right.

Warby Parker is the textbook case for retail as a primary channel, not an afterthought. It built toward roughly 900 locations and used them to expand profitability and accelerate customer growth at exactly the moment online-only peers were stalling. The lesson is that owned retail, when treated as core from early and built deliberately, turns the halo effect into a durable advantage. Warby isn't a DTC brand with some stores. It's an omnichannel brand whose stores do real acquisition and brand work, and the financials show it.

Vuori teaches the wholesale lesson, and it's a sharp one. Its leadership has been explicit that the omnichannel approach, wholesale included, is their best answer for expanding profitably and accretively to the brand, and they've used wholesale partners to enter new markets like the UK and Japan where a cold paid-acquisition push would have been brutally expensive. Wholesale was on track to grow far faster than DTC and to become the majority of brand sales. The takeaway: wholesale isn't a downgrade from direct, it's the cheapest way into markets and customers DTC can't efficiently reach.

On and HOKA teach the both-engines lesson, that the goal isn't to pick DTC or wholesale but to grow both at once. On grew DTC and wholesale roughly in parallel, both up around 40% in a recent quarter, while HOKA pushed toward $2B in sales with DTC and wholesale each growing strongly. These are performance brands that scaled by refusing the either/or framing entirely. They built DTC for margin and data and wholesale for reach and volume, and let the two reinforce each other instead of competing.

Glossier teaches the cautionary version of the same lesson. It rode DTC and community further than almost anyone, then had to add wholesale through Sephora and expand its own retail to keep growing once the pure-play model plateaued. The lesson isn't that Glossier failed, it's that even the strongest DTC-native brand eventually hit the ceiling and had to add channels to push through it. The brands that did it proactively, on their own timing, fared better than the ones that did it reactively under pressure. That's the entire argument for treating omnichannel as a deliberate sequence rather than an emergency, and for studying the unit economics of your specific category before you assume your brand is the exception.

Strip away the categories and the same shape appears every time. Each brand used DTC to launch, validate, and own the customer, then added wholesale for reach, retail for halo and loyalty, and marketplaces or distribution for incremental volume, in roughly that order. None of them got to scale on paid acquisition alone, and none of them abandoned direct. The brands that struggled, Allbirds and Casper, were the ones that treated physical channels as a reluctant afterthought rather than a core part of the architecture. The omnichannel winners didn't have a secret growth hack. They had a better channel portfolio, built in the right sequence.

Why hybrid models

command the

best multiples.

When it's time to sell, the omnichannel work pays a second dividend, because hybrid models earn the highest multiples in the category. Brands that combine DTC, marketplaces, and retail frequently trade around 5x to 7x EBITDA, and omnichannel operators command multiples roughly 15% to 25% higher than single-channel peers. Buyers pay that premium for a simple reason: diversified revenue is worth more than fragile revenue, and they've been burned enough by the fragile kind to price the difference in.

The logic is risk, not romance. A brand that's 80% dependent on Meta is one algorithm change, one CPM spike, one policy shift away from a completely different P&L, and every sophisticated buyer knows it. A brand whose revenue is spread across DTC, wholesale, retail, and marketplaces can absorb a shock in any one channel without the whole business breaking. That resilience is exactly what a buyer is underwriting, so they pay more for it. The same EBITDA dollar is worth more inside a diversified, defensible model than inside a single-channel one that could evaporate, which is the same principle that governs what makes a DTC brand sellable at all.

There's a data dimension too, and it cuts both ways. Buyers prize the first-party data and customer relationships that DTC and owned retail give you, often valuing data-rich brands meaningfully above wholesale-only peers. So the ideal isn't to abandon DTC for wholesale; it's to keep the owned channels that generate the data and the relationship, and add the wholesale and marketplace channels that diversify the revenue. The brand that has both, owned customer data and diversified revenue, is the one that gets the top of the range, because it offers the buyer control and resilience at the same time.

This is why the channel architecture you build for growth is the same one that maximizes your exit. The omnichannel mix that lets you scale past $100M, lower blended CAC, higher retention, diversified revenue, owned data, is precisely the profile that a strategic or financial buyer pays a premium for. You're not doing two separate jobs, building the business and prepping it for sale. You're doing one job well, and the sale value follows. The brands that command the headline multiples in consumer M&A are almost never pure-play, and that's not a coincidence.

For an enterprise acquirer, the calculus is sharper still. A strategic buying a brand wants distribution it can plug into and a customer base it can't easily replicate, and a hybrid brand offers both: established wholesale relationships and retail presence the strategic can scale, plus owned DTC data the strategic can't get from a wholesale-only target. That combination is why the same forces reshaping how enterprises lose ground to DTC challengers also make hybrid challengers the most attractive acquisitions when those enterprises decide to buy rather than build.

The omnichannel path to $100M comes down to a single shift in how you think about channels. Pure-play DTC treats one engine, paid acquisition, as the whole business, and that engine quietly fails somewhere between $20M and $50M as costs rise and audiences saturate. Omnichannel treats DTC as the anchor of a portfolio and adds wholesale, retail, and marketplaces around it, each for a specific job. The result is a structurally lower blended CAC near $40 instead of $120, retention closer to 89% than 33%, diversified revenue that survives a shock in any one channel, and the channel architecture that earns the best multiples on exit. The brands that scaled past the ceiling all did it. The ones that didn't, mostly didn't.

If your brand is parked on the DTC plateau and you're not sure which channel to add next or in what order, that's the exact work I've run from the operator's seat: the blended-CAC model, the first wholesale account, the retail test, the margin math on each. The consumer commerce practice exists for brands at this inflection, and the channel-mix strategy that maps the sequence to your specific numbers is usually the highest-leverage conversation a stalled DTC brand can have.

Questions from founders

stuck on the DTC

plateau.

Because the model runs into a wall on paid acquisition. Customer acquisition costs have climbed roughly 60% over five years, and at $20M to $50M most brands have already maxed out Meta and Google, where ad spend often eats 30% to 40% of revenue. Each new dollar of growth costs more than the last, so the curve flattens. Pure-play DTC can reach eight figures on paid traffic, but pushing toward $100M on that single engine usually breaks the unit economics before it breaks the revenue ceiling.

Materially lower on a blended basis. DTC-only acquisition typically runs $45 to $150 per customer, while brands operating across online, retail, and wholesale together often see blended acquisition land in the $25 to $50 range. The reason is that wholesale and retail buyers don't carry a click cost, and a store builds awareness that lowers the cost of every other channel. You're not replacing paid acquisition; you're diluting it with cheaper sources of customers, which pulls the blended number down.

No, but pure-play DTC as a standalone path to scale is. DTC stays the best place to launch, own the customer relationship, and read demand, and 82% of DTC brands above $50M now run a physical retail presence rather than going online-only. The brands declared dead, Casper and Allbirds among them, weren't killed by DTC itself but by trying to scale it profitably on paid traffic alone. DTC is a channel and a launchpad, not a complete business model at $100M.

Use DTC to validate, then layer deliberately. The pattern that works is roughly: prove demand and own the customer on DTC to about $10M to $20M, add marketplaces and a first wholesale account in the $20M to $40M band, build owned retail and shop-in-shops past $40M, then deepen all four toward $100M. The omnichannel inflection usually hits between $20M and $50M, and almost every $30M-plus brand is planning, building, or rebuilding its first major wholesale or retail push within 24 months.

Because diversified revenue is worth more than fragile revenue. Hybrid models that combine DTC, marketplaces, and retail frequently trade around 5x to 7x EBITDA, and omnichannel operators command multiples roughly 15% to 25% higher than single-channel peers. Buyers pay the premium because revenue spread across four channels survives a shock in any one of them, while a brand that's 80% dependent on Meta is one algorithm change away from a different P&L. The same EBITDA dollar is simply worth more inside a defensible model.

Which channel should your brand add next?

I've run the omnichannel expansion from the operator's seat: the blended-CAC model, the first wholesale accounts, the retail tests, the margin math on each channel. If your brand is stalled on the DTC plateau, I can map the sequence and the numbers for your specific business. The form takes two minutes.

Start a conversation More about Taylor →